Crypto exchanges to avoid if you are Indian in 2026

Jan, 1 2026

Jan, 1 2026

If you're trading crypto in India, picking the wrong exchange isn't just a bad decision-it could cost you everything. You might think all platforms are the same, but that’s not true. Some exchanges are legally risky, others are technically broken, and a few have already lost millions of user funds. In 2026, the rules haven’t changed much, but the consequences have gotten worse. If you're using an exchange that doesn’t follow Indian law, you’re playing with fire-and you won’t get help when it burns you.

Why compliance matters more than you think

India doesn’t ban crypto trading, but it doesn’t protect you either. The Financial Intelligence Unit of India (FIU-IND) is the only body that tracks crypto transactions for anti-money laundering purposes. If an exchange doesn’t register with FIU-IND, it’s operating in the shadows. That means:- Your INR deposits might get blocked by banks without warning

- If the exchange gets hacked, you have zero legal recourse

- You’re on your own for filing 30% capital gains tax and 1% TDS

- The Enforcement Directorate can freeze your bank account just for using it

There’s no official list of compliant exchanges, but FIU-IND has publicly fined major platforms. That’s your clue. If they’ve been fined, they’re not safe. And if they’re not fined yet? That doesn’t mean they’re clean-it means they’re just lucky so far.

Binance: Global giant, local liability

Binance is the biggest crypto exchange in the world. But in India, it’s a liability. In 2023, FIU-IND slapped Binance with a ₹120 crore penalty for failing to register as a reporting entity. The penalty wasn’t just a fine-it was a warning. Binance stopped accepting INR deposits. It stopped helping Indian users with KYC. And it still doesn’t provide tax reports that match Indian law.Many Indian traders still use Binance through third-party payment gateways. That’s risky. If your bank detects a transaction to Binance, they can freeze your account. If FIU-IND investigates, they’ll trace the funds back to you. You didn’t break the law-but you used a platform that did. And in India, that’s enough to trigger a money laundering probe.

Bybit: The silent violator

Bybit is another global exchange that Indian regulators have targeted. In early 2024, FIU-IND fined Bybit ₹85 crore for not reporting user data and not implementing proper AML controls. Unlike Binance, Bybit never even tried to comply. It kept operating, ignoring Indian law. Today, it still doesn’t offer INR on-ramps through Indian banks. It doesn’t provide tax summaries. And it has no customer support team based in India.Traders who use Bybit often report frozen accounts with no explanation. When they reach out, they get automated replies. No phone number. No email response. No timeline. If your funds vanish, there’s no one to call. And Indian authorities won’t step in because Bybit isn’t registered under any Indian financial law.

WazirX: The homegrown disaster

WazirX was India’s biggest exchange. Six million users. $5.4 billion monthly volume. Backed by Binance. Part of the Blockchain India Fund. It looked like the safe choice.Then, in July 2024, it got hacked.

A multi-signature wallet was compromised. $230 million vanished. Not a small amount. Not a glitch. A full-scale collapse. And what happened after? WazirX didn’t return funds. It didn’t shut down. It just stopped communicating. Users were told to wait. Then wait longer. Some got partial refunds after months. Others are still waiting over a year later.

WazirX still lists 250+ cryptocurrencies. It still charges 0.10% to 0.40% trading fees. But it’s not operating like a business. It’s operating like a ghost. And Indian regulators haven’t forced it to return funds. No court order. No public timeline. Just silence.

If you’re holding crypto on WazirX today, you’re holding it on a platform that has already proven it can’t protect your money. And you have no legal protection.

What happens when your funds are frozen?

Imagine this: You log in. Your balance is gone. You email support. No reply. You call. No one answers. You check Twitter. The exchange posted a vague update: “We’re working on it.”That’s the reality on non-compliant exchanges. There’s no consumer protection law for crypto in India. No ombudsman. No dispute resolution. No deadline. You’re at the mercy of a foreign company with no accountability to Indian courts.

Even if you’re not doing anything illegal, using these platforms makes you a target. The Enforcement Directorate has already raided homes and seized bank accounts of crypto users who traded on Binance and Bybit. They don’t need proof of crime. Just using a non-compliant platform is enough to start an investigation.

Tax nightmares: You’re on your own

India taxes crypto profits at 30%. Every sale over ₹50,000 triggers 1% TDS. That’s not optional. You have to report it.Compliant exchanges like CoinDCX and ZebPay auto-generate tax reports. They label your trades. They show your cost basis. They export to Excel or CSV in a format that matches Indian tax software.

Non-compliant exchanges? They don’t do any of that. You have to track every single trade manually. Buy. Sell. Swap. Stake. Airdrop. That’s thousands of transactions. One mistake, and you underpay. The tax department can go back up to six years. A single error could mean penalties, interest, and legal notices.

There’s no excuse for this in 2026. If an exchange can’t give you a tax report, it’s not fit for Indian users.

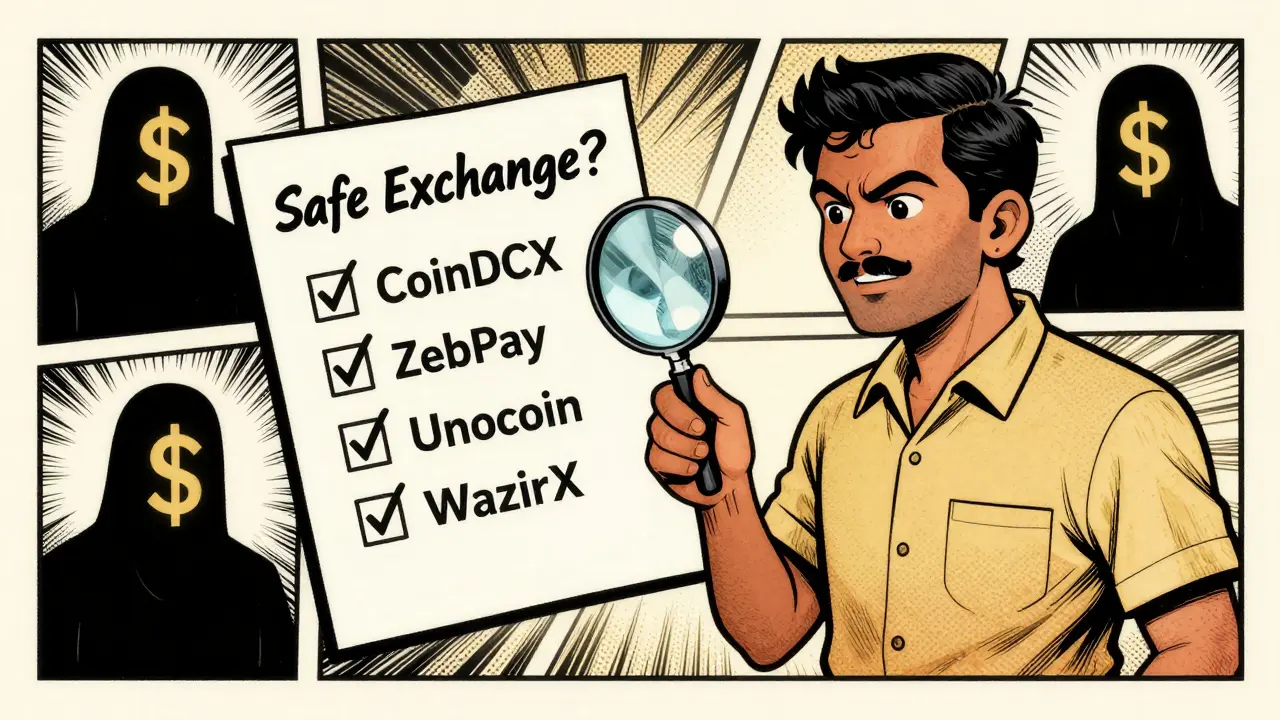

What to use instead

You don’t need to avoid crypto. You just need to avoid the bad platforms. Stick to exchanges that have shown they’re trying to comply:- CoinDCX: Registered with FIU-IND, offers INR deposits, provides tax reports

- CoinSwitch Kuber: Works with Indian banks, has customer support in India

- ZebPay: One of the first to register with FIU-IND, transparent about compliance

- Unocoin: Long-standing platform, supports TDS reporting

- Bitbns: Local team, regular updates on regulatory status

These aren’t perfect. They’ve had downtime. They’ve had delays. But they’re trying. They answer emails. They update their websites. They don’t vanish after a hack.

How to check if an exchange is safe

Before you deposit money, ask these questions:- Is the exchange registered with FIU-IND? (Check their website for a compliance page)

- Can you deposit INR directly through UPI or bank transfer? (If not, they’re avoiding regulators)

- Do they provide a downloadable tax report? (Test it with a small trade)

- Is there a live chat or Indian phone number? (No support = no accountability)

- Have they been fined by Indian authorities? (Search “FIU-IND fine [exchange name]”)

If the answer to any of these is “no,” walk away. Even if it has low fees or cool tokens. Your money isn’t worth the risk.

The bottom line

Crypto isn’t illegal in India. But using the wrong exchange might be. Binance, Bybit, and WazirX aren’t just risky-they’ve already been punished by Indian regulators. And the people who lost money? They’re still waiting. No refunds. No answers. No justice.You don’t need to chase the biggest names. You don’t need to gamble on unregulated platforms. There are safe, local options that work. Use them. Protect your money. Stay compliant. And don’t let greed make you ignore the warning signs.

Is it legal to trade crypto on Binance in India?

Trading crypto itself is legal in India, but using Binance is risky. Binance was fined ₹120 crore by FIU-IND for not registering as a reporting entity. It doesn’t offer INR deposits, doesn’t provide tax reports, and has no customer support for Indian users. Using it could trigger an Enforcement Directorate investigation, even if you’re not doing anything illegal.

Why did WazirX lose $230 million?

WazirX lost $230 million in July 2024 after a hacker compromised its multi-signature wallet. The exchange didn’t have proper security controls or real-time monitoring. After the hack, it stopped returning funds and started restructuring. Over a year later, most users still haven’t been fully refunded, and there’s no clear timeline or legal action forcing them to pay back.

Can Indian banks block my account for using crypto exchanges?

Yes. Banks in India classify non-FIU-compliant exchanges as high-risk. If they detect transfers to Binance, Bybit, or WazirX, they can freeze your account without warning. You’ll need to prove your transactions were legal, which is hard without proper tax records. Even compliant exchanges like CoinDCX have had temporary blocks, but they help users resolve them.

Do I have to pay tax on crypto even if I use a non-compliant exchange?

Yes. India’s 30% capital gains tax and 1% TDS apply regardless of which exchange you use. Non-compliant platforms don’t report your trades, so you’re responsible for tracking every transaction manually. Failing to file can lead to penalties, interest, and legal notices from the tax department-even if you didn’t break any crypto rules.

Are there any Indian crypto exchanges that are completely safe?

No exchange is 100% risk-free, but CoinDCX, CoinSwitch, ZebPay, Unocoin, and Bitbns are the safest options. They’re registered with FIU-IND, support INR deposits, provide tax reports, and have Indian customer support. They still face regulatory uncertainty, but they’re the only ones trying to follow the rules. Avoid any exchange that doesn’t clearly state its compliance status.

Jordan Fowles

January 2, 2026 AT 16:03It's wild how the legal gray zones in crypto just turn ordinary people into unintentional criminals. You're not laundering money, you're not scamming anyone-you're just trying to invest. But the system doesn't care about intent. It cares about compliance, and compliance is a moving target written in bureaucratic legalese. The real tragedy? The people who get punished aren't the ones designing the loopholes. They're the ones trying to survive in a system that never asked for their permission to be this complicated.

Steve Williams

January 4, 2026 AT 09:42While I appreciate the thoroughness of this analysis, I must emphasize the importance of regulatory adherence as a cornerstone of financial integrity. The absence of formal registration with FIU-IND renders any platform legally untenable within the Indian jurisdiction, regardless of its global stature. Prudence dictates that users align their digital asset activities with statutory frameworks to mitigate systemic risk and preserve personal financial sovereignty.

nayan keshari

January 5, 2026 AT 16:04Bro this whole post is just fearmongering. Binance has been around longer than most Indian exchanges. You think the government’s gonna shut them down? Nah. They’re just playing hardball. And yeah, WazirX got hacked, but that’s because they were lazy with security, not because they were illegal. I’ve been on Bybit for 3 years, never had a problem. Tax? I file it myself. Stop scaring newbies with drama.

Jackson Storm

January 5, 2026 AT 21:40Okay so I get why you're mad about Binance and Bybit but lemme ask you this-have you actually tried getting a tax report from CoinDCX? I did last month and their CSV was missing 17 trades. Like, what’s the point of a 'compliant' exchange if they still botch the basics? And don’t even get me started on ZebPay’s app crashing every time you try to withdraw. They’re better? Maybe. But they’re not perfect. You gotta do your own tracking, no matter who you use. Don’t trust the platform, trust your spreadsheets.

Raja Oleholeh

January 7, 2026 AT 19:28Foreign exchanges stealing our money and laughing? 🤬 Time to ban them all. India doesn’t need Binance. We have CoinDCX. We have Unocoin. We have our own. Why let a foreign company play with our rupees? If you use Binance, you’re not trading crypto-you’re betraying your own country. 🇮🇳🔥

Michelle Slayden

January 8, 2026 AT 11:04The philosophical underpinning of this piece is not merely regulatory compliance-it is the assertion of individual agency within a state apparatus that remains ambivalent toward emerging financial technologies. The absence of legal protection is not an oversight; it is a deliberate policy of non-engagement. To participate is to accept a form of sovereign abandonment. One must ask: Is financial autonomy worth the psychological burden of perpetual legal vulnerability?

Haritha Kusal

January 9, 2026 AT 06:10i know its scary but i just keep my money on coinswitch and try not to think about it too much. i dont wanna lose everything but i also dont wanna miss out. its like walking on thin ice but at least the ice is from india 😅

Mike Reynolds

January 10, 2026 AT 07:19I’ve used Binance for years. Never had my bank freeze. Never got fined. I file my taxes manually. I’ve got spreadsheets going back to 2020. Yeah, they don’t help you-but you don’t need them. You just need to be organized. This whole post feels like a PSA from someone who got scared after one bad experience. Don’t let fear make you miss out on the best platform out there.

dayna prest

January 11, 2026 AT 14:51Let’s be real-this isn’t about compliance, it’s about control. The government doesn’t want you to have decentralized money. They want you to be dependent on banks, on taxes, on paperwork. So they paint Binance as the villain and hand you CoinDCX like a lollipop. But here’s the twist: the lollipop’s made of sugar-coated bureaucracy. You think you’re safe? You’re just trading one cage for another. The real crypto revolution? It’s still underground.

Brooklyn Servin

January 13, 2026 AT 08:45Okay, I’m done pretending this is a fair fight. You want to know what’s really dangerous? The fact that Indian regulators have zero transparency. No public registry of compliant exchanges. No official list. No hotline. Just ‘check their website’ like that’s enough. Meanwhile, Binance has 24/7 support, multi-sig wallets, and insurance. And you’re telling me to trust CoinDCX because they ‘try’? Try harder. If you’re not holding your keys, you’re not owning crypto. And if your ‘safe’ exchange can’t even give you a tax report that works? That’s not safe-that’s a dumpster fire with a UPI logo.

Willis Shane

January 13, 2026 AT 14:18Your argument rests on the assumption that regulatory compliance equates to security. This is a fallacy. Compliance ensures visibility to authorities, not protection from hackers or insolvency. WazirX was compliant for years. It still collapsed. Binance, while non-compliant in India, maintains robust infrastructure and global insurance. The real issue is not legality-it is systemic resilience. To equate regulatory adherence with safety is to confuse procedure with substance.

Jake West

January 15, 2026 AT 00:57LMAO so you’re telling me I can’t use Binance because they got fined? Bro, that’s like saying don’t use Netflix because they got fined for copyright stuff. Everyone breaks rules. The real question is: does it work? Does it have liquidity? Can you withdraw? Does it have 2000 coins? Yeah? Then shut up and trade. This post reads like a government pamphlet written by someone who’s never bought a crypto in their life.

Gavin Hill

January 16, 2026 AT 11:36Compliance is a word the government uses to scare people into trusting the system. But the system doesn’t protect you. Banks freeze accounts. Tax notices arrive out of nowhere. The exchanges that get fined? They’re the ones who tried to play ball. The ones that didn’t get fined? They’re still running. So who’s really safe? Nobody. Just be smart. Use a cold wallet. Track your trades. Don’t put all your money on one platform. And don’t believe anyone who says they’ve got the answer.

SUMIT RAI

January 16, 2026 AT 17:21WazirX got hacked? LOL imagine trusting a local exchange with your life savings 😂 Binance is still the only one that actually works. I use a VPN, I use a friend’s bank account, I file my own taxes. I’m not scared. I’m smarter than the system. 🤷♂️