Virtual Digital Assets Taxation in India: Complete Guide for 2026

Feb, 8 2026

Feb, 8 2026

India’s rules around Virtual Digital Assets (VDAs) taxation aren’t just complicated-they’re designed to make crypto investing feel like a high-stakes game with strict penalties for mistakes. If you’re buying, selling, or holding Bitcoin, Ethereum, NFTs, or any other digital asset in India, you’re playing by rules that changed dramatically in 2022 and got even tighter in 2025. Forget what you know about capital gains from stocks or real estate. VDAs operate under a completely different system-one that doesn’t care if you held your Bitcoin for two days or two years. The tax rate is always 30%. No exceptions. No deductions. No loss offsets. And if you’re not careful, you’ll get hit with 1% TDS on every transaction over ₹10,000. Here’s the cold truth: if you’re making money from crypto in India, the government is taking 30% of your profit before you even see it. And if you lose money? Tough luck. You can’t use those losses to reduce your tax bill on your salary, your business income, or even your stock market gains. The system doesn’t let you balance the books. It treats every crypto trade like a standalone bet-with no safety net. Let’s break it down, step by step, so you know exactly what you’re up against-and what you can still do about it.

What Counts as a Virtual Digital Asset?

The Indian government didn’t leave room for guesswork. Under Section 2(47A) of the Income Tax Act, a Virtual Digital Asset is anything that:- Isn’t Indian or foreign currency

- Exists as digital code, token, or data

- Has value or functions as a store of value or unit of account

- Can be transferred, stored, or traded electronically

The 30% Flat Tax: No Exceptions

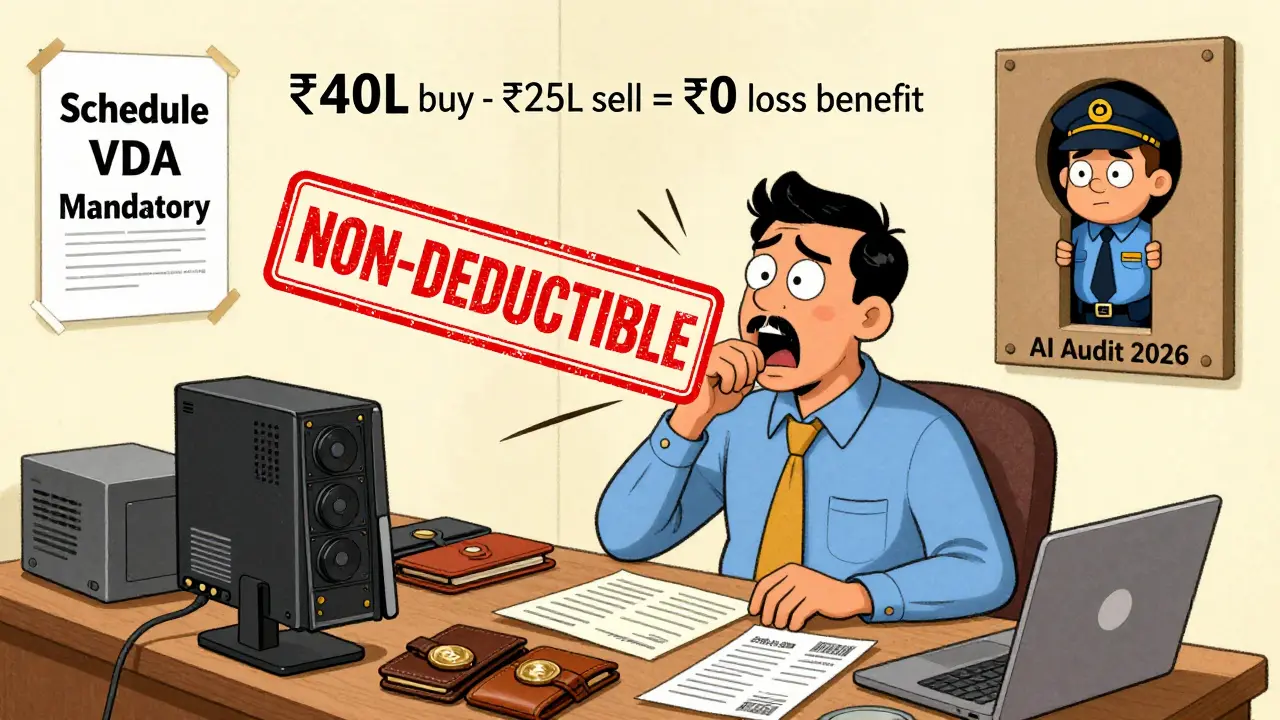

Section 115BBH of the Income Tax Act says it plainly: all gains from VDAs are taxed at 30%. No matter your income slab. No matter how long you held the asset. No matter if you’re a day trader or a long-term holder. The tax rate is fixed. Compare that to stocks or real estate. With stocks, if you hold for over a year, you pay just 10% on gains above ₹1 lakh. With real estate, long-term gains get indexation benefits that cut your tax burden by nearly half. With VDAs? None of that. You get 30%-period. And here’s the kicker: the only thing you can deduct is the cost of acquisition. That means the price you paid to buy the asset. Everything else? Gone. Transaction fees? Not deductible. Gas fees on Ethereum? Not deductible. Mining equipment costs? Not deductible. Even the fees you paid to transfer crypto from one wallet to another? Irrelevant. The tax department only cares about what you paid to buy it and what you sold it for.Losses Can’t Offset Anything

This is where most investors get blindsided. If you bought Bitcoin at ₹40 lakh and sold it at ₹25 lakh, you lost ₹15 lakh. You might think, "Great, I can use this loss to reduce my taxable income from my job or my stock gains." Nope. Under Section 115BBH, losses from VDAs cannot be set off against any other income. Not salary. Not business income. Not capital gains from stocks or property. Not even gains from other VDAs in the same year. The only thing you can do is carry forward the loss-for eight years. And even then, you can only use it to offset future VDA gains. So if you lost ₹15 lakh this year, you can only apply it against profits you make from crypto in the next eight years. If you never make another profit? That loss disappears. It’s like a tax write-off with an expiration date you can’t control.TDS: 1% on Every Big Transaction

If you’re trading on Indian exchanges like WazirX, CoinDCX, or ZebPay, you’ve probably noticed a 1% deduction on your withdrawals or sales. That’s Tax Deducted at Source (TDS) under Section 194S. It kicks in when:- You’re a regular person (non-specified person) and your total VDA transactions exceed ₹10,000 in a financial year

- You’re a specified person (like someone with annual income under ₹1 crore) and your transactions exceed ₹50,000

How to Report VDAs in Your Tax Return

You can’t ignore this. If you traded VDAs in FY 2025-26, you must file ITR-2 or ITR-3. You can’t use ITR-1. In the return, you’ll fill out Schedule VDA. You need to report:- Date of acquisition

- Date of transfer

- Cost of acquisition

- Full value of consideration (sale price)

- TDS deducted

What You Can’t Deduct (And Why It Matters)

Let’s say you spent ₹50,000 on mining rigs, paid ₹15,000 in gas fees, and spent ₹20,000 on a crypto tax software. Under normal rules, you’d deduct these as business expenses. But for VDAs? Not allowed. The government’s logic is simple: VDAs are treated as investments, not businesses. So unless you’re running a crypto mining company as a registered business, you can’t claim any operating costs. This hits miners and DeFi traders hard. If you earn crypto through staking or liquidity pools, that income is taxed as “other income” at your slab rate. Then, when you later sell it, you pay another 30% on the gain. You’re taxed twice-once on the income, once on the profit. No double taxation relief. No credits. Just two layers of tax.Real-World Impact: Who’s Getting Hurt?

The numbers don’t lie. According to KPMG’s 2023 survey, 68% of institutional investors cut their Indian crypto exposure by half after the new rules. BlackRock’s India team said it made the country non-competitive for global crypto funds. Individual investors aren’t faring much better. On Reddit, users like "CryptoSaverIN" posted about losing ₹2.87 lakh on Ethereum and being unable to offset it against their ₹18 lakh salary. That’s a ₹5.4 lakh tax bill on the salary alone, while the crypto loss vanished. Trustpilot reviews show 62% of complaints on Indian exchanges are about TDS errors-over-deductions of 15-22%. Some users got charged TDS on transfers between their own wallets. Others were charged twice on the same trade. The system is automated, but it’s not smart.

What People Are Doing to Adapt

Despite the harsh rules, people are still trading. Why? Because the returns can still be massive. A WalletInvestor survey found 61% of users keep trading because they believe the upside outweighs the tax hit. Here are the workarounds people are using:- Gifting to family members: If your spouse or parent is in a lower tax bracket, you can gift VDAs to them. When they sell, they pay tax on the gain. This is legal, as long as you don’t get the money back.

- Using ETFs: Some traders are shifting from direct crypto to Bitcoin ETFs (when available). These are taxed as securities, not VDAs. That means long-term gains get indexation benefits. One Reddit user claimed a 3.2% higher net return by switching.

- Timing sales: Selling in a year when your salary income is low can help minimize the impact of the 30% tax.

What’s Changing in 2026?

The Income Tax Act, 2025, which came into effect in August 2025, didn’t change the 30% rate. But it did make two big shifts:- Tax Year replaces Financial Year: Your tax period now aligns with the calendar year (January-December), not April-March. This matches global norms and simplifies reporting for international traders.

- Digital-first enforcement: The tax department now uses AI to cross-check wallet addresses, exchange data, and blockchain records. If your transaction history doesn’t match your return, you’ll get a notice-no warning.

What You Need to Do Now

If you’re active in crypto in India, here’s your checklist:- Track every transaction: Use a crypto tax tool like Koinly or CoinTracker. Export your history from every exchange and wallet.

- Save proof of purchase: Screenshots of buy orders, transaction IDs, wallet addresses. If the tax department asks, you need to prove what you paid.

- Report all income: Staking rewards, airdrops, mining income-all taxable. Don’t assume they’re "gifts" or "free money."

- Check your TDS: Log into your exchange account and download Form 26QE. Match it with your transaction history.

- File ITR-2 or ITR-3: Don’t use ITR-1. Schedule VDA is mandatory.

- Keep records for 8 years: The tax department can audit you anytime within that window.

Final Reality Check

India’s VDA tax system isn’t designed to encourage crypto adoption. It’s designed to capture revenue. And it’s working. The government collected ₹3,920 crore in FY2023-24-27% more than expected. By FY2025-26, projections say it could hit ₹9,200 crore. The trade-off? Simplicity for the government, complexity for the user. No more guesswork on tax rates. But also no more flexibility. No loss offsets. No deductions. No mercy. If you’re still trading, you’re either betting big on future price surges-or you’re already paying the tax premium and hoping the returns make it worth it. There’s no perfect solution. But if you’re smart, you’ll treat this like a business. Track everything. Plan ahead. And don’t assume the system will be kind.Are NFTs taxed the same as Bitcoin in India?

Yes. Any NFT-whether it’s a digital artwork, a game item, or a collectible-is classified as a Virtual Digital Asset under Indian law. When you sell an NFT for a profit, you pay 30% tax on the gain. The cost of acquisition (what you paid to buy it) is the only deduction allowed. If you bought an NFT with cryptocurrency, the value of the crypto you used is treated as your acquisition cost. If you received an NFT as a gift or airdrop, its fair market value at the time of receipt becomes your cost basis.

Can I avoid TDS by using a foreign exchange?

Technically, yes-if you trade only on non-Indian exchanges and don’t transfer funds to an Indian bank account, TDS won’t be deducted. But here’s the catch: the Indian tax department can still track your transactions through bank records, forex reporting, and global data-sharing agreements. If you’re an Indian resident, you’re still required to report all global VDA gains in your tax return. Avoiding TDS doesn’t mean avoiding tax. It just means you’ll have to self-report and pay manually, with no automatic deduction. The risk of audit increases.

What happens if I don’t report my crypto gains?

The tax department now has direct access to data from all Indian exchanges. They know who bought, sold, and transferred crypto. If you don’t report, you’ll get a notice. Penalties include a fine of up to 200% of the unpaid tax, interest at 1% per month, and possible prosecution for tax evasion. In FY2023-24, over 12,000 crypto-related notices were issued. Ignorance is not a defense.

Can I claim losses from crypto scams or hacks?

No. Even if your wallet was hacked or you fell for a scam, the loss cannot be claimed as a tax deduction. The tax department does not recognize theft or fraud as a valid reason to offset gains. You’ll still owe tax on any profits you made in the same year, and the loss from the hack disappears. This is one of the harshest aspects of the rule-there’s no protection for victims of fraud.

Is staking or mining crypto taxable in India?

Yes. Rewards from staking, liquidity pools, or mining are taxed as "other income" at your applicable income tax slab rate when you receive them. If you later sell those coins, you pay another 30% on the gain. For example, if you earn 0.5 ETH from staking worth ₹2 lakh, you pay tax on ₹2 lakh at your slab rate. If you later sell that ETH for ₹2.5 lakh, you pay 30% on the ₹50,000 gain. You’re taxed twice-once on income, once on capital gain.

mahikshith reddy

February 8, 2026 AT 20:0230% tax on crypto? Bro, this is just India finally growing up. No more free rides. If you want to gamble on moon coins, pay the price. The system isn't broken-it’s working exactly as intended. Stop crying and start accounting.

And yeah, NFTs? Same rules. Stop thinking you’re special because you bought a monkey picture.

Brendan Conway

February 9, 2026 AT 03:35so like… if i lose money on crypto, i still gotta pay 30%? that’s wild. in usa we can offset losses. this feels like the gov just wants your cash no matter what. kinda sad lol.

Katie Haywood

February 10, 2026 AT 08:52Ohhh so that’s why my friend’s TDS was 15% on a wallet transfer… classic Indian exchange glitch. They’re not dumb, they’re just overworked. The system’s a mess, but at least it’s consistent. 30% is brutal, but hey-at least you know where you stand. No surprises. That’s something, right? 😅

Jesse Pasichnyk

February 10, 2026 AT 11:06Let me get this straight-India taxes crypto like it’s a lottery ticket? No deductions? No loss offsets? Bro, that’s not taxation, that’s punishment. We’re not in a socialist state anymore, we’re in a crypto police state. 🇮🇳🔥

orville matibag

February 12, 2026 AT 05:24As someone who’s lived in both India and the US, I get why they did this. Crypto was becoming a tax evasion playground. People were moving money under the radar. The 30% is harsh, but it’s clean. No loopholes. No gray zones. You want to play? Pay the fee. Simple. No drama.

And yes, gifting to family? That’s the smart move. Not a loophole. A family strategy. Like sending money to a kid’s college fund.

Josh Flohre

February 13, 2026 AT 23:01Let’s be clear: if you’re using crypto to avoid taxes, you’re not a visionary-you’re a criminal. India’s system is transparent, predictable, and fair. You pay 30%. You get no deductions. You can’t offset losses. So what? That’s not oppression. That’s accountability. If you can’t handle that, maybe you shouldn’t be trading.

Oliver James Scarth

February 15, 2026 AT 15:42One cannot help but observe that India’s VDA taxation framework exhibits a remarkable degree of administrative clarity. While the absence of loss-offset mechanisms may appear draconian to Anglo-American sensibilities, it is, in fact, a deliberate design to eliminate speculative arbitrage and enforce fiscal discipline. The 1% TDS is not a burden-it is a telemetry system. Every transaction is now traceable. This is not taxation as coercion. It is taxation as governance.

And to those who moan about NFTs being taxed the same as Bitcoin: if both are digital assets with fungible value, why should their fiscal treatment differ? The state does not care for your aesthetic preferences-it cares for revenue integrity.

Kieren Hagan

February 17, 2026 AT 01:49For anyone considering crypto trading in India: document everything. Every transaction. Every wallet address. Every timestamp. The IT department now has AI-powered blockchain trackers. If you’re not keeping records, you’re not just risking penalties-you’re risking legal exposure.

Use Koinly. Export your history. Save screenshots. Keep proof of purchase. This isn’t optional. It’s your only defense.

sachin bunny

February 18, 2026 AT 14:48lol 30% tax? nah bro… this is all a scam. The government is working with the exchanges to drain our wallets. They already know who owns what. They’re building a digital surveillance state. Next thing you know, they’ll freeze your wallet if you buy too much BTC. 🤡💸

Udit Pandey

February 20, 2026 AT 06:59As an Indian citizen who has paid taxes for 18 years, I find this system not just fair, but noble. Crypto was never meant to be a tax-free haven. It was always meant to be a speculative tool for the unregulated. Now, it’s regulated. And rightly so.

Those who complain about losing ₹15 lakh on Ethereum and not being able to offset it? You didn’t lose ₹15 lakh. You lost ₹15 lakh on a gamble. That’s not a loss-it’s a lesson. The tax code doesn’t reward poor judgment. It rewards discipline.

And yes, I know people say, "But in America, you can offset!"-so what? We’re not America. We’re India. We don’t import your fiscal philosophies. We build our own.

Stop comparing. Start complying. The system is clear. The rules are simple. Pay 30%. Keep records. File ITR-2. That’s it. No drama. No excuses.

Ajay Singh

February 22, 2026 AT 03:28bro just use ETFs if you want to chill. 30% sucks but at least you can sleep at night. no audit nightmares. no TDS errors. just buy and forget. simple. 😎

Michelle Anderson

February 23, 2026 AT 05:09"You’re taxed twice on staking?" Oh honey. Welcome to reality. You think crypto is magic? It’s just money with extra steps. The government doesn’t owe you tax breaks because you "mined" coins in your basement. You’re not a pioneer-you’re a taxpayer. Get over it.

Matt Smith

February 23, 2026 AT 13:4230% tax? Bro, that’s not a tax-it’s a robbery with paperwork. 😭 And TDS on transfers between YOUR OWN wallets? That’s not enforcement, that’s incompetence. I’ve seen more logic in a vending machine. 🤡

Olivette Petersen

February 23, 2026 AT 16:36It’s not about the tax. It’s about the clarity. Before, no one knew what was legal. Now? You know exactly what you owe. That’s power. Yeah, 30% hurts. But at least you’re not hiding. You’re not cheating. You’re playing the game. And if you’re smart? You’ll use the rules to your advantage. Gifting. ETFs. Timing. It’s all doable. You just have to be strategic.

Ryan Chandler

February 24, 2026 AT 12:52India didn’t ban crypto. They didn’t ignore it. They didn’t pretend it didn’t exist. They looked it in the eye and said: "You’re money. You’re taxable. You’re not special."

That’s leadership. That’s courage.

Most countries are still arguing over whether crypto is money, a commodity, or a security.

India just taxed it. And moved on.

Shruti Sharma

February 25, 2026 AT 18:42so i just lost 50k on a hack and still have to pay 30% on my other gains? lol this is insane. who designed this? some guy in a suit who’s never even seen a wallet? 🤡

Alex Garnett

February 27, 2026 AT 14:31Let’s be honest-this system was designed to crush retail crypto traders. The 30% flat rate, no loss offsets, TDS on every transaction-it’s not fiscal policy. It’s economic suppression. The government doesn’t want you to get rich. It wants you to stay poor and compliant. And if you’re smart? You’ll move your assets offshore. Because this isn’t taxation. It’s extortion dressed in a tax form.